Sikkim PUBLIC FINANCE and Fiscal Policy

Basic Understanding of Public Finance of Sikkim

Public finance as a concept may be understood on two levels –

- as a practical activity of all components of Public Administration and

- As a theoretical area.

- The term “public finance“ may be defined as the identification of specific financial relationships and functions running between public administration bodies and institutions (i.e. public sector entities – the state) as one party and in mutual interaction with other entities of the economic system as the other party (i.e. private entities – households and companies).

- These relationships and functions may be considered special as they include:

- Procuring public goods (production and provision);

- arranging and funding various transfers (particularly in the social area);

- Directing entities existing in the economy towards socially desirable behaviours; for instance through taxes, penalties, subsidies and other stimuli and charges.

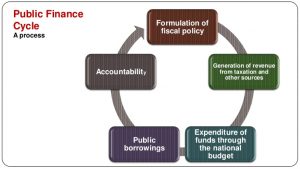

- In order to arrange the funding of the above-mentioned areas, there is a Fiscal System (public BUDGETING system) whose aim is to collect the required amount of public revenue. Public revenue serves, at various levels of public budgets (governmental, regional and local), to fund public expenditures.

- Public expenditures, public revenue and particularly taxes may be considered to be the fundamental Elements of public finance. Important terms derived from these three elements include deficit, Public Debt, budgetary policy and fiscal policy.

- The development of public finance is connected with economic mechanisms that should ideally lead to the effective and fair allocation of limited Resources.

Public Finance – Causes of Development Aspects of Sikkim

- The reason for developing public funding is the state intention to soften the drawbacks resulting from economic decisions made by individual entities (households and companies). It uses fiscal tools (public revenue and expenditure) to accomplish this.

- Certain behaviour is classified as the “quasi-fiscal funding principle”, where publiclaw goods are funded from off-budgetary resources (e.g. the public-law television in the Czech Republic is funded from television licence fees).

- Another important term that relates to public finance, and that is also a strong argument for its development, is market failure.

- The market system follows supply and demand through the price mechanism. It is a system that has developed itself, and that has strong ties with the interactions between people and companies.

- All these entities strive to maximize their benefit (welfare). The greatest benefit is strongly interconnected with reaching the economic optimum condition.

- A system that reaches the optimum is considered, in the neoclassical economics concept, to be efficient, fair and stable.

- The ideal condition is called the Pareto optimum. This exists in an economy when none of the involved entities can improve its position without worsening another entity’s position. If any of the entities intends to improve its position, it is possible for it to do so only to the detriment of another entity. The existence of perfect competition is a necessary requirement for reaching the optimum.

- The three above-mentioned elements (efficiency, stability and fairness) are connected with microeconomics from the viewpoint of efficiency, connected with macroeconomics from the viewpoint of stability, and connected with sciences outside economics from the viewpoint of fairness. The perception of fairness is investigated by other social sciences, and is closely linked to ethics, etc.

- If no conditions exist for reaching a market-efficient solution, or the conditions are simply violated for any reason, market failure will ensue.

- It consists of the following:

- The allocation of resources is not efficient,

- The economy in the area of macroeconomics indicators oscillates around the desired values and

- The distribution of wealth and income may diverge from the consensus on fairness.

- It is then up to the state to perform its fiscal function (the public finance function) in those three areas in order to preferably eliminate or at least reduce market failure. Specifically, those are microeconomic failures from the allocation function perspective, macroeconomic failures from the stabilization function perspective, and the redistribution function then falls into the area of market failure caused by outside economies.

- If the conditions for perfect competition are not met, a malfunction in the price mechanism will arise, which disturbs the allocation mechanism. Some failures can be eliminated without public finance intervention through auto-regulation (the internalization of externalities). However, others are part of the government’s allocation function and its fiscal tools (taxes and governmental purchases or transfers).

- Macroeconomic failure is indicated by instability in the economic system that usually suffers from cyclical Inflation, a high rate of Unemployment, low or even negative Growth of production or problems in the Foreign Trade balance, etc.

- The above-mentioned macroeconomic cases of instability are why governments perform the state stabilization functions (stabilization fiscal functions).

- The state uses several tools to perform the stabilization function. The basic Classification is a division into monetary and fiscal tools. The monetary tools include open market operations, the setting of basic interest rates, determining the level of mandatory minimum reserves, etc. Fiscal tools may include public expenditure, public revenue and ways of funding deficits.

- The causes of market failure outside the economy relate to reaching fairness in Society through the distribution of wealth and income. With the distribution of wealth, the market does not practically perceive fairness. In this case, the state performs a redistributive role with 5h3 principles of solidarity, social conscience, charity, etc. based on the social consensus.

- The state performs the redistribution function through two basic categories of tools. The first includes revenue (tax) and the other expenditures (transfers, grants and subsidies).

- First, a tax transfer mechanism may be implemented through a combination of Taxation/”>Progressive taxation of high incomes and transfers (subsidies) in favour of low income households.

- Secondly, this can occur through the taxation of luxury goods combined with subsidies on goods for the low-income Population.

Fiscal Policy Meaning

- Arthur Smithies defines fiscal policy as “a policy under which the government uses its expenditure and revenue programmes to produce desirable effects and avoid undesirable effects on the NATIONAL INCOME, production and EMPLOYMENT.”

- Though the ultimate aim of fiscal policy in the long-run stabilisation of the economy, yet it can be achieved by moderating short-run economic fluctuations.

- In this context, Otto Eckstein defines fiscal policy as “changes in taxes and expenditures which aim at short-run goals of full employment and price-level stability.

Objective of Fiscal Policy

- To maintain and achieve full employment.

- To stabilise the price level.

- To stabilise the growth rate of the economy

- To maintain equilibrium in the Balance of Payments.

- To promote the Economic Development of underdeveloped countries

Revenue Receipt Aspects of Sikkim

- Tax Revenue Comprises taxes collected and retained by the State and State’s share of union taxes under ARTICLE 280(3) of the Constitution.

- Non-Tax Revenue Includes interest receipts, dividends, profits etc. Grants in Aid and Contributions

- Grants-in-aid represent central assistance to the State Government from the Union Government. Includes ‘External Grant Assistance’ and ‘Aid, Material & Equipment’ received from Foreign Governments and channelised through the Union Government. In turn, the State Government also gives Grants-in-aid to Panchayati Raj Institutions, Autonomous Bodies etc.

Expenditure Aspects of Sikkim

- Expenditure is classified as Revenue Expenditure (which is used to meet the day-to-day running of the Government), and Capital Expenditure (which is used to create permanent assets, or to enhance the utility of such assets or to reduce permanent liabilities). Expenditure is further classified under Plan and Non-plan across different Services viz., General services, Social services and Economic Services.

- General Services Includes Justice, Police, Jail, PWD, Pension etc.

- Social Services Includes Education, Health & Family Welfare, Water Supply , Welfare of SC-ST etc.

- Economic Services Includes agriculture, Rural Development, Irrigation, Cooperation, Energy, Industries, Transport etc.

Medium Term Fiscal Plan for Sikkim: 2016-17

Introduction – Fiscal Policy Overview

- The fiscal year 2016-17 is the second year of the award period of the 14th Finance Commission (FFC). The fiscal Stress faced by the State in the year 2015-16 persisted in 2016-17 as well.

- The fiscal challenges faced by the State necessitated modifications in the financing pattern based on the changes in resource transfers by the Central Government.

- The share of Sikkim in the divisible pool of Central taxes has been raised to 0.367 per cent as compared to the share of 0.239 recommended by the 13th FC.

- The increase in State’s and rise in the divisible pool of Central taxes from 32 to 42 percent due to the recommendations of the FFC has resulted in higher tax devolution to the State. However, rise in tax devolution subsumed many grants to the State and overall Central transfer was declined last year.

- However, the State Government is committed to improve the provision of the public services and protect the spending on priority sectors while being prudent in fiscal management.

- The Sikkim Fiscal Responsibility and Budget Management Act of 2010 (FRBM Act) provides the benchmark for fiscal management in the State.

- The FRBM Act was enacted in the State with the objective of providing fiscal stability and conducting the fiscal policy in a sustainable manner to reduce the deficit and stabilize the debt burden.

- It is expected that a rule based fiscal policy will establish long run fiscal sustainability improving the credibility of the Government policy and focus on spending to build social and physical Infrastructure-2/”>INFRASTRUCTURE.

- Given that the State has a limited base to generate resources internally and the provision of public services in a difficult hilly terrain is costly, the Government needs to calibrate it fiscal policy and spending pattern with a restraint provided through the fiscal rules.

- The State Government, over the years, managed to adhere to the fiscal targets, while adopting a development oriented fiscal policy. The overall fiscal management in terms of budget decisions and implementation has remained within the boundary set in the fiscal rules.

- The fiscal adjustment path for Sikkim recommended by the Thirteenth Finance Commission (TFC) with targeted Fiscal Deficit to ensure sustainable level of debt ended at 2014-15.

- The FRBM Act of the State took into account the recommendations made by the 14th Finance Commission starting from the fiscal year 2015-16.The FFC recommended certain changes in the Fiscal Consolidation process to provide flexibility in the fiscal management of the State.

- The State Government has brought amendments this fiscal to the State FRBM Act reflecting these recommendations.

- The development oriented fiscal management over the years helped the State Government achieving socio-economic development and an Inclusive Growth process. Creating an enabling Environment for different sections of the society, different tribal groups, Women, and young people to participate in economic activities and contribute to the development of the State has remained as major objectives of the Government

Achievement of social sector commitments

- Achievement of social sector commitments constitutes an important element of resource allocation decisions in the context of rule based fiscal policy that restricts incurring deficit and borrowing to a sustainable level. The Gross State Domestic Product (GSDP) at constant prices recorded a healthy growth rate of 7.88 percent in 2013-14.

- The per capita income of the state, which was Rs.30727 in 2004-05, has increased substantially to Rs.196144 in 2016-17 at current prices. The major socioeconomic indicators for the State show commendable improvement.

- The POVERTY ratio has declined to 8.19 per cent as compared to all India Average of 21.92 per cent in 2011-12. The Literacy rate at 81.40 per cent in 2011-12 is significant achievement. The IMR has gone down to 24 per 1000 in 2011 as compared to the all India average of 44.

Macroeconomic Outlook of Sikkim

- The CSO has not updated the GSDP data of Sikkim for the year 2014-15. For all projection purposes, the method suggested by the FFC has been adopted to update the GSDP. The State GSDP, during 2012-13 and 2013-14, grew consistently at a reasonable rate of 7.6 and 7.9 per cent respectively.

- While the service sector dominated the State income during 2005-06 to 2008-09, the share of Industry sector started increasing since 2009-10 and in 2013-14 the service sector constituted about 60.6 per cent of the total GSDP.

- The relative share of industry sector has increased mostly driven by manufacturing, construction and power sectors. The inter-sectoral composition of GSDP since 2004-05 shows that the service sector, which accounted for half of the State GSDP till 2008-09, has declined to about 30 per cent in 2013-14.

- The relative share of agriculture sector, which comprises of agriculture, Forestry and fishing, has been declining over the years. The share of agriculture sector has come down from about 14 per cent in 2008-09 to 9.5 per cent in 2013-14.

- The manufacturing and construction sectors remained as major contributors to the growth of the State economy. The year 2009-10 marks a clear shift in the growth path of the GSDP as the growth rate in this year jumped to a high of 73.6 per cent (89.9 per cent in current prices).

- The impressive growth of power sector was basically driven by generation of hydroelectricity in newly commissioned power projects.

- The manufacturing sector showed very high growth due to higher production in pharmaceutical industries and strengthening of small-scale industries. The manufacturing sector constitutes about one third of the State GSDP in 2013-14.

- The initial burst in the growth of power and manufacturing sectors has stabilized in recent years. However, this established a strong base for the GSDP in Sikkim.

Fiscal Profile of the State

The Changing Fiscal Architecture and Its Impact on Sikkim

- The budget for the year 2016-17 was the second budget after the FFC gave its recommendations on devolution of resources to the States. Despite the rise in share of Sikkim in tax devolution, aggregate transfers to the State declined in 2015-16 relative to GSDP due to sharp decline in grants.

- Based on the tax devolution share for Sikkim and grants recommended by the FFC, the State received less central transfers in 2015- 16 as compared to 2014-15. The loss of assured source of block grants has created fiscal stress for the State and it seems unlikely that the increased tax devolution would compensate for this.

- The FFC increased tax devolution to the State from 32 per cent to 42 per cent to provide higher flexibility in the use of enhanced level of untied fund.

- As the FFC relied on tax devolution to cover the assessed revenue expenditure needs of the States, it took a holistic view of the revenue expenditure needs of States without Plan and Non-Plan distinction.

- The FFC departed from past practice by not awarding specificpurpose grants. These grants, according to the Commission, were small to make any impact and crate confusion where large Plan schemes already exist, and were left to the Centre and the states acting cooperatively for those needs. The only grants awarded by the Commission were disaster relief grants and grants for local bodies.

- The Commission was required by their terms of reference to recommend grants for these two purposes. The commission steered clear of both the Plan/Non-Plan distinction and that between special-category and other states.

- Consequent upon the enhancement of share of the states in the central divisible pool from the current 32 percent to 42 percent which is the biggest ever increase in vertical tax devolution, Central Assistance to State Plan has been restructured.

- The Central Government has discontinued the normal central assistance (NCA), special plan assistance (SPA), special central assistance (SCA), and the additional central assistance (ACA).

- The Central Government also delinked eight centrally sponsored schemes (CSS) from funding and brought about substantial changes in the funding pattern of some other schemes.

- The higher growth rate assumed by the FFC resulted in higher assessed revenue of the State during the award period of the Commission.

- The own tax revenue projected for 2015-16 by the Commission is Rs 876.00 crore (calculation is based on GSDP of Rs 20634 crore), which rises to Rs.3039 crores in the year 2019-20.

- Higher tax projection by the Commission reduced the pre-devolution Revenue Deficit gap for the State during the award period. The FFC projected Revenue Receipts seems to be unachievable.

- The FFC transfer to the State also depends on the resource mobilization by the Central Government. While the FFC recommended Rs.2129 crores as share in Central Taxes to Sikkim, the Union budget for 2015-16 provided Rs.1929 crores only.

- The actual flow however, was much less at Rs.1870 crores. This implies a gap of Rs.259 crores, which is expected to grow in the future years unless the the Central taxes increases considerably.

- Decline in Central Grants and the gap in actual flow of tax devolution to that of the budget projection makes it very difficult to provide funds to the infrastructure projects started earlier based on the fund flow mechanism existing under the then Planning Commission and the Finance Commission.

Expenditure Profile

- The Government of Sikkim has successfully controlled the revenue expenditure as Percentage to GSDP. This has helped the State to increase the revenue surplus and expand the capital expenditure.

- The priority sectors in social and economic services were traditionally given emphasis in resource allocation. The State Government has initiated several schemes in education and health to improve overall social and human infrastructure in the State.

- The revenue expenditure, which was at 29.8 per cent relative to GSDP in 2009-10, was compressed to 23.12 per cent in 2014-15 and was budgeted at 23 percent in 2016-17. While the level of expenditure on social and economic services was protected in 2015-16 as compared to the previous year, the level of spending relative to GSDP projected for the year 2016-17 was low.

- The expenditure compression in 2016-17 was due to lower availability of resources.

Outstanding Debt and Government Guarantee

- Maintaining the debt burden of the State at sustainable level remains one of the major objectives of the fiscal management of the State as reflected in the FRBM Act.

- The TFC in their revised fiscal roadmap have worked out the yearly outstanding debt burden for all the states aligning with the fiscal path.

- The debt-GSDP ratio in the State has been reduced considerably, which is projected to be 23 per cent in 201617 BE.

- The decline in the average cost of debt of the state because of the debt restructuring formula of the Twelfth Finance Commission has helped to lowering the debt burden.

- Decline in the average cost of debt will result in reduction in the volume of interest payments and availability of higher fiscal space for the state government.

- The interest payment has declined from 2.5 per cent in 2009-10 relative to GSDP to 1.6 per cent in 2016-17 (BE).

Medium Term Fiscal Plan: 2016-17 to 2018-19

Fiscal Indicators

- The fiscal outcomes in the form of indicators like fiscal deficit, revenue deficit, and outstanding liabilities for previous year, current year, ensuing budget year and two outward years are presented.

- The fiscal outcomes of the year 2014-15, for which audited figures are available, show that the State Government has adhered to the fiscal targets under the Act. In the year 2015-16, the Government took the benefit of flexibility provided by the FFC to raise the fiscal deficit to 3.25 percent to GSDP.

- However, due to slippage in revenue receipts, the fiscal deficit has increased to 3.31 percent. The budget projections of the year 2016-17, however, show that the fiscal deficit has been contained at 3 percent of the GSDP. The Government managed to generate revenue surplus all along.

- The projections for the budget year, 2016-17, and for two outward years, which give a medium term perspective to the fiscal stance, is aligned with the FRBM Act. The MTFP from 2016-17 to 2018-19 conforms to the recommendations of the FFC to anchor the fiscal deficit to 3 per cent of GSDP.

- The MTFP 2016-17 presents the outlook of the fiscal management of the State Government in the medium term. The detailed projection of fiscal variables show that the revenue account surplus has been maintained during the MTFP period and the fiscal deficit has been stabilized at 3 per cent relative to the GSDP.

- Despite reducing the revenue expenditure from 23 percent relative to GSDP to about 22.3 percent, the revenue surplus could not be increased due to low growth of revenues relative to the GSDP.

- While GSDP is assumed to grow at 17.69 percent, the total revenue receipt grow at about 16 percent. The loss of block grants has pulled down the aggregate revenue receipts.

- In nominal terms the revenue surplus increases from Rs.260.51 croers in 2016-17 (BE) to Rs.359.81 crores in 2018-19. Despite rise in fiscal deficit in nominal terms, it remains at 3 percent of GSDP, the mandatory requirement under the FRBM Act. The outstanding liabilities declines from 23.18 percent in 2016-17 BE to 22.29 percent in 2018-19.

- As indicated, due to higher growth of GSDP, the fiscal variable in the medium term show a lower value. However, there has been substantial growth in revenue receipts and allocations to various sectors in nominal terms. While revenue receipts increases from Rs.4885 crores to Rs.6580 crores in the medium term, the revenue expenditure rises from Rs.4625 crores to Rs.6221 crores. The growth of revenue expenditure remains below the growth revenues.

- The provision for capital outlay has increased from Rs.847 crores to Rs.1178 croers during MTFP period. Relative to GSDP, the capital outlay has shown an increase in the medium term.

- Despite pressure on revenue receipts and competing demands, the focus on investments in infrastructure will remain a key factor in fiscal policy of the Government.

Summary Assessment

- The State of Sikkim continues to face fiscal stress for the second year in a row after the fiscal architecture involving the fiscal federal arrangements have changed following the FFC recommendations.

- As the Central transfers constitute a large portion of the State’s budget, the loss of some of assured source of revenue from plan grants has created difficulties in resource allocation in the State.

- Although, the fiscal indicators show a declining trend due to high growth of GSDP, the nominal numbers show growth in revenues and resource allocation. The growth in resource allocation, particularly in the priority sectors in social and economic series and capital outlay has been restrained.

- This has added increased responsibility on the State Government to generate higher revenue and continue with the traditional policy of emphasizing social and Infrastructure Sectors.

- Despite the pressure on resources, the MTFP indicates a stable and growth oriented fiscal policy for Sikkim. The rise in production of electricity and growth of the manufacturing sector influenced the economic growth of the State in recent years.

- The fiscal policy has to create an enabling environment for further growth and socioeconomic progress.

- The resource allocation in the medium term focuses on enhancing the capital expenditure and social and economic sector spending. The economy needs better infrastructure and Human Development to make progress. The State Government has initiated several schemes in the social and economic sectors in recent years.

- Despite the problem of cost disability, the State is committed to improving the service delivery spanning over the social and economic sector. The MTFP safeguards the fiscal consolidation process and provides adequate resources to existing schemes in priority areas.

- The FFC recommended anchoring fiscal deficit to 3 per cent of the GSDP. The MTFP continues with the fiscal target set for fiscal deficit at 3 per cent. As debt stock in the State relative to the GSDP remains low, the debt-GSDP target remains stabilized. While projecting State taxes, the MTFP assumed higher buoyancy to augment resources, which will be achievable in the medium term.

- The modernization of tax administration and efforts to improve the tax base is expected to improve the revenue receipts. It was observed that there has been some uncertainty in the flow of share in Central taxes. The tax devolution to the State varies depending upon the collection of Central taxes as the Finance Commission recommends a share in the divisible pool.

- In the year 2015-16, against a budgeted amount of Rs.1924 crores, which was also less than what the FFC projected, the transfer to the State was only Rs.1870 crores. This level unpredictability affects State finances adversely.

- The expenditure side restructuring in the MTFP was based on the realties regarding the resource availability and priorities expressed Government’s policies, and new schemes announced in the budget.

- The MTFP protected the capital outlay relative to the GSDP and raised it marginally during the MTFP period. The rise in nominal terms is substantial. The rise in the capital expenditure will be instrumental in strengthening the infrastructure base in the State.

- The State Government will be able to enhance the level of capital expenditure with the improvement in resource position.

- What is important is to develop a policy to focus more on productive capital expenditure. The debt burden of the State remains below the limit suggested by the FFC to gain from the flexibility clause regarding the fiscal deficit.

- The State Government has amended its FRBM Act in 2016-17 to avail the facility of increasing the borrowing limit and consequently the fiscal deficit by 0.25 present separately based on the FFC recommendations.

- This will further help in maintaining the fiscal discipline and stability, adequate resource allocation to social and economic sector and strengthening infrastructure base.

| The highlights of the Budget for the year 2017-18 with a summarized account of the receipts and disbursements incorporated in the budget. | |||||||||||||||||||||||||||||||||||||||

|

,

Public finance is the study of the government’s revenues and expenditures. It is a branch of economics that deals with the financial activities of the government. Public finance is concerned with the raising and spending of government funds, as well as the management of the government’s debt.

Public revenue is the income that the government receives from taxes, fees, and other sources. Tax revenue is the most important source of public revenue. Taxes are compulsory payments that are levied by the government on individuals and businesses. The government uses tax revenue to finance its activities, such as providing public goods and services, and to redistribute income.

Non-tax revenue is revenue that the government receives from sources other than taxes. Examples of non-tax revenue include fees, fines, and profits from government enterprises. Non-tax revenue is a relatively small source of public revenue, but it can be an important source of funding for certain government programs.

Public expenditure is the Money that the government spends on its activities. Public expenditure can be divided into two categories: capital expenditure and recurrent expenditure. Capital expenditure is spending on long-term assets, such as roads, bridges, and schools. Recurrent expenditure is spending on day-to-day activities, such as salaries, pensions, and interest payments.

Fiscal policy is the government’s use of taxation and spending to influence the economy. Fiscal policy can be used to stimulate the economy, to reduce inflation, or to reduce the government’s debt.

Fiscal deficit is the difference between the government’s revenue and expenditure. A fiscal deficit occurs when the government spends more than it receives in revenue. The government can finance a fiscal deficit by borrowing money, which increases the government’s debt.

Public debt is the total amount of money that the government owes. The government’s debt can be financed by borrowing money from domestic or foreign sources. The government’s debt can be a problem if it becomes too large, as it can lead to higher interest rates and inflation.

The Fiscal Responsibility and Budget Management Act (FRBM Act) is an Indian law that was enacted in 2003. The FRBM Act aims to promote fiscal discipline and transparency in the government’s finances. The FRBM Act sets limits on the government’s fiscal deficit and debt.

Fiscal sustainability is the ability of the government to continue to finance its activities without running into financial difficulties. Fiscal sustainability is important because it ensures that the government will be able to meet its obligations in the future.

Fiscal transparency is the openness and clarity with which the government reports its financial information. Fiscal transparency is important because it allows citizens to hold the government accountable for its spending.

In conclusion, public finance is a complex and important topic. It is important to understand the government’s revenues and expenditures, as well as its fiscal policy. Fiscal sustainability and fiscal transparency are also important issues.

What is public finance?

Public finance is the study of the government’s revenues and expenditures. It includes the study of how the government raises money, how it spends money, and how it manages its debt.

What is fiscal policy?

Fiscal policy is the use of government spending and taxation to influence the economy. The government can use fiscal policy to stimulate the economy during a Recession or to slow down the economy during a period of high inflation.

What are the different Types of Taxes?

There are many different types of taxes, but some of the most common include income taxes, sales taxes, and property taxes. Income taxes are taxes on the income that people earn from work, investments, and other sources. Sales taxes are taxes on the goods and services that people buy. Property taxes are taxes on the value of real estate that people own.

What are the different Types of government spending?

Government spending can be divided into two main categories: discretionary spending and mandatory spending. Discretionary spending is spending that is authorized by Congress each year. Mandatory spending is spending that is required by law, such as Social Security and Medicare.

What is the national debt?

The national debt is the total amount of money that the government owes. The government borrows money by selling Treasury Bonds. The national debt has been growing in recent years, and it is now over $30 trillion.

What are the benefits of public finance?

Public finance can help to stabilize the economy, provide essential services, and redistribute income.

What are the drawbacks of public finance?

Public finance can be inefficient, lead to Corruption, and increase the national debt.

What are some examples of public finance?

Some examples of public finance include the Social Security program, the Medicare program, and the Federal Reserve System.

What are some of the challenges facing public finance?

Some of the challenges facing public finance include the aging population, the rising cost of healthcare, and the increasing national debt.

What are some of the solutions to the challenges facing public finance?

Some of the solutions to the challenges facing public finance include raising taxes, cutting spending, and reforming entitlement programs.

Sure, here are some MCQs on the topic of public finance and fiscal policy:

Which of the following is not a component of public finance?

(A) Revenue

(B) Expenditure

(C) Debt

(D) TaxationWhich of the following is not a function of government?

(A) Providing public goods and services

(B) Regulating the economy

(C) Redistributing income

(D) Collecting taxesWhich of the following is not a type of tax?

(A) Income tax

(B) Sales tax

(C) Property tax

(D) Excise taxWhich of the following is not a fiscal policy tool?

(A) Taxation

(B) Spending

(C) Monetary Policy

(D) Deficit spendingWhich of the following is not a goal of fiscal policy?

(A) To stabilize the economy

(B) To promote economic growth

(C) To reduce unemployment

(D) To redistribute incomeWhich of the following is not a characteristic of a progressive tax system?

(A) The tax rate increases as income increases

(B) The tax base is broad

(C) The tax is equitable

(D) The tax is efficientWhich of the following is not a characteristic of a regressive tax system?

(A) The tax rate decreases as income increases

(B) The tax base is narrow

(C) The tax is inequitable

(D) The tax is efficientWhich of the following is not a characteristic of a proportional tax system?

(A) The tax rate is the same for all taxpayers

(B) The tax base is broad

(C) The tax is equitable

(D) The tax is efficientWhich of the following is not a reason for government debt?

(A) To finance wars

(B) To finance infrastructure projects

(C) To stimulate the economy

(D) To redistribute incomeWhich of the following is not a risk of government debt?

(A) Inflation

(B) Default

(C) Crowding out private Investment

(D) Higher taxes in the future

I hope these MCQs were helpful!